The Asymmetric Position Sizing Strategy: A 2026 Playbook For Retail Swing Traders

Studying indicators and chart patterns yet still losing money? The issue isn’t your entry; it’s your capital commitment.

As per SEBI’s official data, 93% of over 1 crore individual F&O traders lost an average ₹2 lakh each (FY22-FY24), with aggregate losses exceeding ₹1.8 lakh crore. Only 1% earned profits over ₹1 lakh after transaction costs.

Recent market conditions make risk management critical. Algorithmic participation creates faster price movements and sharper reversals that punish undisciplined traders. This is where asymmetric position sizing becomes valuable: predefined rules that align position size with risk, conviction, and reward potential.

A strong system with fluctuating position sizes based on confidence will lose money. Average entries with disciplined risk management often achieve consistent performance. Asymmetric position sizing removes guesswork from capital allocation, ensuring every trade is evaluated objectively before money is at risk.

Why Most Swing Traders Struggle Despite Good Setups

Many retail traders assume technical analysis is the missing piece. They continuously search for better indicators, more accurate chart patterns, and advanced market theories that promise improved profitability.

The reality is that most traders already know enough about entries. Their results suffer because they fail to manage risk consistently once a position is active.

A trader may risk 1% on one setup and 5% on another simply because the second trade feels more convincing. Over time, this emotional sizing creates unnecessary volatility in account performance. This is exactly where structured risk management strategies become critical in maintaining consistency.

The asymmetric position sizing strategy addresses this problem by replacing subjective decisions with mathematical rules. Instead of reacting emotionally, traders follow a predefined framework for every trade.

Another common mistake occurs after a winning streak. Confidence increases, position sizes expand, and traders begin taking risks they would normally avoid. One oversized loss then erases weeks of progress. The opposite also happens. After a series of losses, traders become fearful and reduce exposure dramatically. When a strong setup finally appears, they are too cautious to benefit from it.

What Makes The Asymmetric Position Sizing Strategy Different

Traditional position sizing methods often treat every trade equally. Traders risk the same amount regardless of setup quality, market conditions, or expected reward potential.

While this approach introduces consistency, it does not account for the fact that some opportunities are objectively better than others.

The asymmetric position sizing strategy recognizes these differences. It allows traders to allocate capital more efficiently while maintaining strict risk controls.

For example, a high-conviction setup with a tight stop loss and a strong reward profile may justify larger exposure than a lower-quality opportunity with uncertain potential.

This does not mean taking excessive risk. The asymmetric position sizing strategy still operates within predefined account-level risk limits.

The difference is that exposure is adjusted based on opportunity quality rather than applied uniformly across all trades.

As a result, traders concentrate capital where probabilities are strongest while reducing exposure when conditions become less favorable.

The asymmetric position sizing strategy also improves decision-making. Once rules are established, there is no need to debate position size before every trade.

The calculation becomes objective. This reduces emotional interference and helps traders remain focused on execution. Over time, this structured approach can significantly improve both consistency and confidence.

The 5-Step Framework For Implementing Trading Risk Management Strategies

Successful execution requires more than understanding the concept. Traders need a repeatable process that can be applied to every opportunity.

The following framework helps traders implement the asymmetric position sizing strategy in a practical and disciplined manner.

Step 1: Define Maximum Risk Per Trade

The first step is determining the maximum amount that can be lost on any single trade. This number should be based on current account equity rather than emotions.

Many experienced swing traders limit risk to 1% of account value per trade. This approach protects capital while allowing room for normal market fluctuations.

For example, a trader with a ₹10 lakh account may decide that ₹10,000 is the maximum acceptable loss on any position.

This rule becomes the foundation of the asymmetric position sizing strategy because every future calculation depends on a predefined risk limit. By making this decision before market hours begin, traders eliminate impulsive adjustments during periods of volatility.

Step 2: Determine Stop Loss Before Position Size

A common mistake among retail traders is calculating position size first and then deciding where the stop loss should go. This often results in arbitrary stop placement designed to justify larger positions rather than protect capital.

A better approach is to identify the invalidation level before calculating exposure. The stop should be placed where the trade idea becomes invalid.

Once the stop is established, position size can be calculated accurately. This ensures risk remains controlled regardless of market conditions. The asymmetric position sizing strategy relies heavily on this step because accurate sizing is impossible without a predefined exit level.

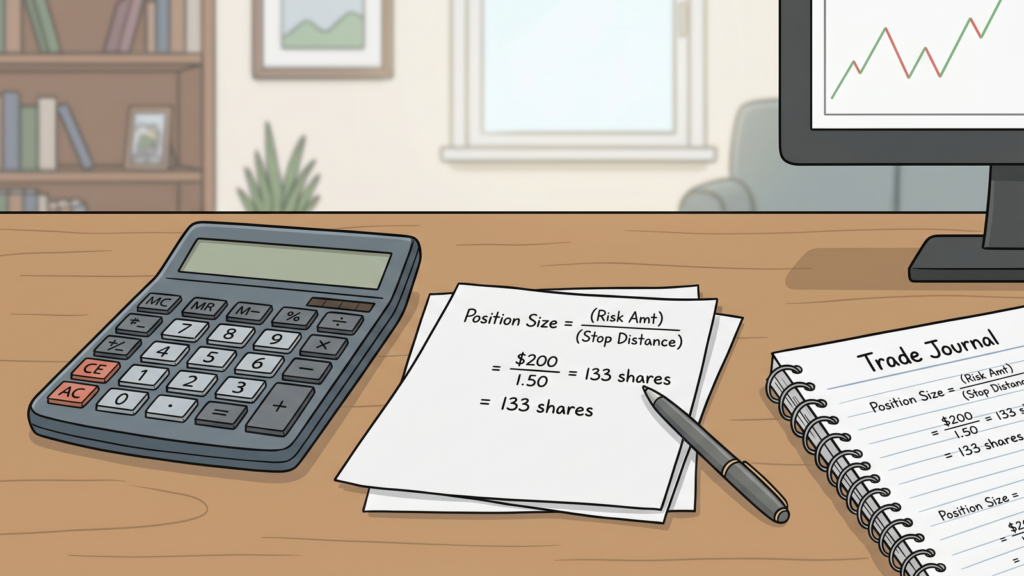

Step 3: Calculate Position Size Using Fixed Risk

After defining account risk and stop distance, position size becomes a simple calculation.

Position Size = Maximum Account Risk ÷ Stop Distance

Suppose a trader is willing to risk ₹10,000 and the stop loss is ₹20 away from entry. The resulting position size would be 500 shares. This calculation ensures every trade carries the same monetary risk regardless of volatility.

The asymmetric position sizing strategy removes uncertainty from this process. Rather than guessing how much to buy, traders simply follow the formula. This creates consistency and prevents emotional decisions during trade execution.

Step 4: Focus Only On High Reward Opportunities

Not every setup deserves capital allocation. One of the most powerful aspects of the asymmetric position sizing strategy is its emphasis on selectivity. Many successful traders require a minimum reward-to-risk ratio before entering any position.

A trade offering a 1:1 reward profile may not justify participation, while a setup offering 1:3 or 1:4 becomes much more attractive. By filtering opportunities through this lens, traders improve overall expectancy without increasing risk.

The asymmetric position sizing strategy encourages capital concentration on opportunities with the strongest potential outcomes. This allows traders to maximize efficiency while maintaining disciplined risk management.

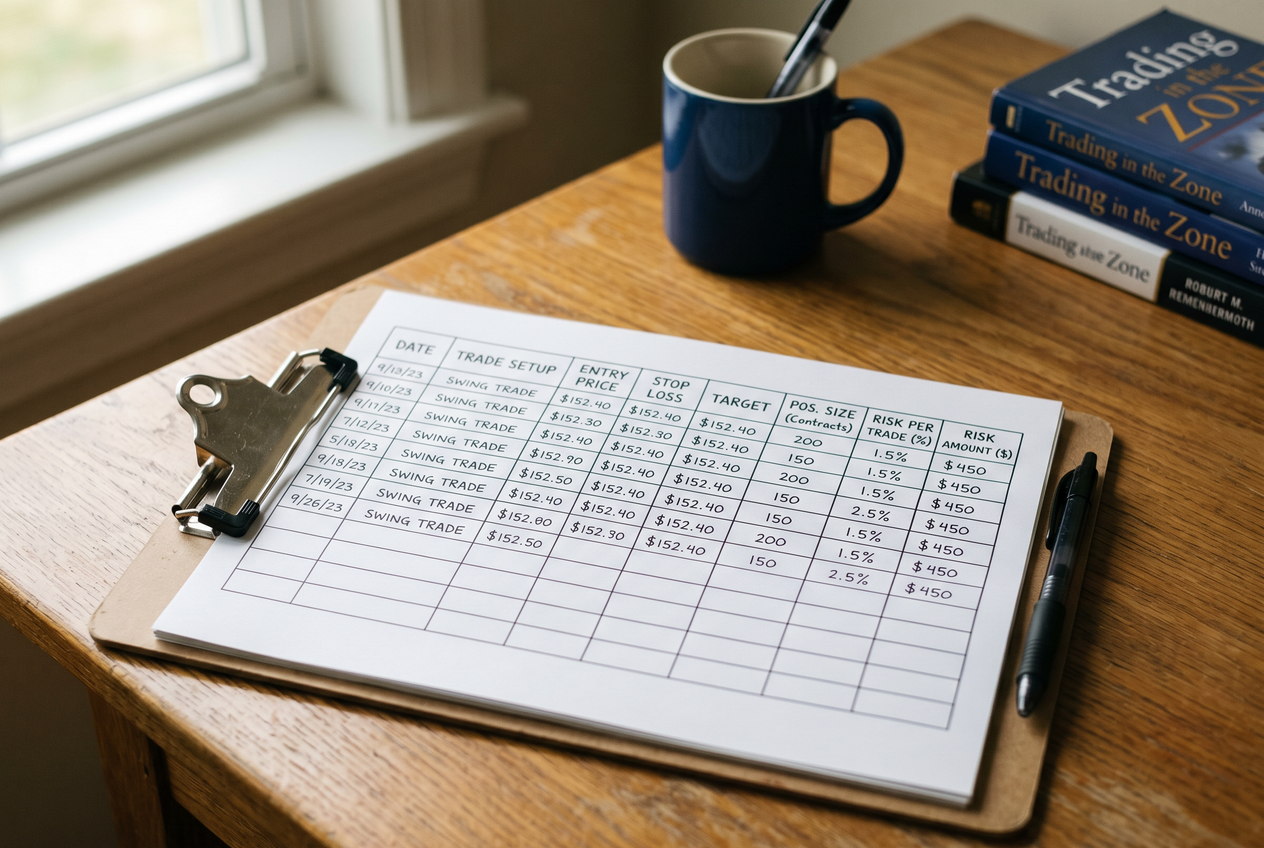

Step 5: Review Every Trade Weekly

Long-term improvement requires consistent review. Traders should track position size, stop placement, reward-to-risk ratio, and execution quality for every trade.

This process reveals recurring mistakes that may otherwise go unnoticed.

A weekly review also helps traders determine whether they are following their own rules consistently. The asymmetric position sizing strategy becomes significantly more effective when supported by detailed performance analysis. Over time, this feedback loop strengthens discipline and improves execution quality.

How Manas Arora Helps Traders Build Risk Management Systems

Many traders understand risk management conceptually but struggle to apply it consistently in live market conditions. Through his educational content and practical frameworks, Manas Arora helps traders bridge the gap between theory and execution.

His systems focus on building repeatable habits that improve decision-making and reduce emotional interference.

Rather than relying on motivation, traders learn how to create processes that support consistent performance across different market environments.

The asymmetric position sizing strategy forms a core part of this philosophy because position sizing influences every aspect of trading performance.

Through structured frameworks, journal templates, risk calculators, and execution checklists, traders develop habits that support long-term success.

For traders seeking consistency rather than excitement, these systems provide a practical path toward sustainable improvement.

Explore our courses here!

Frequently Asked Questions

How Do You Calculate Position Size In Trading?

Position size is calculated by dividing the amount you are willing to risk by the distance between entry and stop loss. The asymmetric position sizing strategy uses this formula to maintain consistent risk across trades.

Should Traders Increase Size After A Winning Streak?

No. Position size should be determined by predefined rules rather than recent outcomes. The asymmetric position sizing strategy helps traders avoid emotional adjustments after wins.

Why Is Stop Loss Discipline Important For Swing Traders?

Stop losses define maximum risk before entering a trade. Without them, traders expose themselves to unpredictable losses that can significantly damage capital.

How Does Trading Psychology Affect Position Sizing?

Fear and overconfidence often influence position size decisions. The asymmetric position sizing strategy reduces emotional interference by replacing subjective decisions with mathematical rules.

Can The Asymmetric Position Sizing Strategy Work For Small Accounts?

Yes. The principles remain identical regardless of account size. The asymmetric position sizing strategy focuses on percentage-based risk, making it scalable across different account values.